By Eric Rife, CFP®, CPWA® and Thomas Pudner, CPA, CFA, CFP®, MST Co-Chief Investment Officer and Co-Director of Research, Mason Investment Advisory Services

If you hold a large, concentrated equity position, you already know the risk. A disproportionate amount of wealth tied to a single stock means a single company’s fortunes have an outsized influence on your financial future. The question most executives face is not whether to diversify — it is how to do so without triggering a tax bill that consumes a significant portion of the gain they have spent years building.

For the right investor, a Section 351 Exchange offers one of the most compelling answers available. It allows you to contribute appreciated stock into a diversified ETF, gain broad market exposure, and defer the capital gains that would otherwise be recognized in a direct sale — all while retaining an investment you can trade freely from day one.

This post is the second in Mason’s concentrated stock series. For an overview of all six strategies available to executives managing a concentrated position, start by reading 6 Strategies to Diversify a Concentrated Stock Position and What Each One Costs You in Taxes. >>

What Is a Section 351 Exchange?

A Section 351 Exchange is a transaction in which an investor contributes a basket of stocks, ETFs, or treasury bills in exchange for shares of a newly created diversified ETF. The name comes from Section 351 of the Internal Revenue Code, which governs tax-deferred transfers of property to a corporation in exchange for stock.

In plain terms: rather than selling your concentrated stock and paying capital gains taxes on the proceeds, you contribute that stock directly into an ETF. In return, you receive shares of that ETF. Your tax basis in the new ETF carries over from the shares you contributed, meaning the gain is deferred rather than recognized at the time of the exchange.

The resulting ETF can be bought and sold on a public exchange like any other ETF, with no lock-up period and no restrictions on when you can access your investment.

How Is a Section 351 Exchange Different from an Exchange Fund?

This is one of the most common questions investors ask when they first encounter the Section 351 Exchange, and the distinction matters significantly.

An exchange fund pools concentrated stock from multiple investors into a single diversified fund. In return for contributing your stock, you receive shares of the fund. Capital gains are deferred, but the trade-offs are substantial: lock-up periods of seven years are required to maintain tax-deferred treatment, fees can be high, the fund must hold at least 20% of its assets in illiquid qualified assets such as private real estate, and the fund is not obligated to accept your contribution if it already holds too much of the same stock.

A Section 351 Exchange is a one-time event rather than an ongoing fund structure. After the exchange, you hold shares of a diversified ETF that trades on a public exchange. There is no lock-up period. There is no requirement to hold illiquid assets. However, similar to the exchange fund, a fund manager may say no to certain holdings or limit how much of a specific security they want to accept.

For investors who have explored exchange funds and been deterred by the illiquidity, the fees, or the seven-year commitment, the Section 351 Exchange often represents the more practical and flexible alternative.

How Does a Section 351 Exchange Work?

The mechanics are more straightforward than the name suggests. Here is the process step by step.

Step 1. Contribute a basket of stocks, ETFs, or treasury bills

Rather than contributing a single concentrated position, investors contribute a basket of securities — their concentrated stock alongside other positions, ETFs, or treasury bills — to seed a new diversified ETF. The basket approach is what enables the transaction to qualify for tax-deferred treatment under Section 351.

Step 2. Pass the diversification test

To qualify for tax-deferred treatment, the basket of stocks and ETFs contributed must pass a two-part diversification test:

- No single stock may exceed 25% of the total contribution.

- The top five stocks used to fund the investment may not be greater than 50% of the total contribution.

One important note: when an ETF is included in the contribution, the diversification test looks through to the underlying holdings of that ETF rather than treating it as a single position. This creates planning opportunities for investors who hold large ETF positions alongside individual stocks.

Step 3. Receive shares of the new diversified ETF

In exchange for the contributed basket, the investor receives shares of the newly created diversified ETF. The tax basis in the new ETF equals the tax basis of the shares contributed, preserving the deferred gain. The investor receives a separate tax lot for each position contributed, which can have meaningful implications for future tax planning.

Step 4. Hold, trade, or incorporate into a broader portfolio

Once the exchange is complete, the investor holds shares of a diversified ETF that can be traded on a public exchange at any time. The ETF can be incorporated into an existing portfolio or serve as a component of a newly constructed diversified managed portfolio.

Section 351 Exchange Examples

The diversification test is easiest to understand through examples. The following scenarios illustrate how the test is applied in practice.

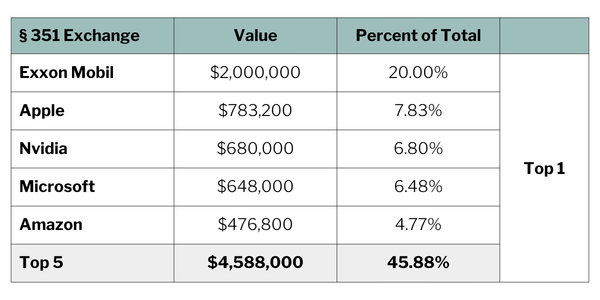

Example 1: ETF plus individual stock

An investor holds $8,000,000 in QQQ, an ETF that tracks the NASDAQ 100 Index, and $2,000,000 in Exxon Mobil stock. For purposes of the diversification test, the position in QQQ looks through to its underlying holdings. Apple, Nvidia, Microsoft, and Amazon are the largest holdings of QQQ, so the 25% and 50% tests are applied as if the investor held those underlying stocks directly.

For example, Apple makes up 9.79% of QQQ. An $8 million investment in QQQ therefore equates to holding $783,200 of Apple stock for purposes of the diversification test. Because no single underlying stock exceeds 25% of the total $10 million contribution and the top five positions do not exceed 50%, this contribution qualifies for tax-deferred treatment.

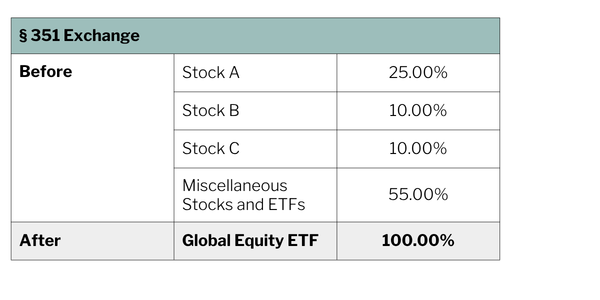

Example 2: Multiple individual stocks and ETFs

An investor holds large concentrations in three individual stocks alongside a basket of other ETFs and individual positions. The investor contributes $2.5 million of Stock A, $1 million of Stock B, $1 million of Stock C, and $5.5 million of miscellaneous stocks and ETFs — a total contribution of $10 million.

Stock A represents 25% of the total contribution, exactly at the limit. The top five positions do not exceed 50% of the total. This contribution meets the diversification requirements, and the investor receives shares of the new ETF valued at $10 million with tax-deferred treatment on the contributed gains.

Who Is a Good Candidate for a Section 351 Exchange?

The Section 351 Exchange is a powerful tool, but it is not right for every investor or every situation. It tends to work best for investors who meet several of the following conditions.

- You hold a large appreciated stock position with a low cost basis and a significant embedded gain that you would prefer not to recognize in the near term.

- You want broad market diversification but are not looking to liquidate your position outright.

- You are comfortable holding the resulting ETF for the long term, understanding that the deferred gain will eventually be recognized when you sell ETF shares.

- You are not primarily motivated by philanthropic goals, which may be better served by charitable strategies such as a Donor Advised Fund or a Charitable Remainder Trust.

- You have been deterred by the illiquidity and structural complexity of exchange funds and are looking for a more flexible alternative.

The Section 351 Exchange is also worth considering for investors who have significant holdings in large-cap ETFs like QQQ alongside individual stock positions, given the look-through treatment that can make diversification test compliance more achievable than it might appear at first glance.

Important Considerations and Limitations

As with any sophisticated tax and investment strategy, the Section 351 Exchange comes with nuances that deserve careful evaluation before proceeding.

Availability is limited. Section 351 Exchanges are structured around specific ETF launches and arise periodically rather than continuously. While not all fund families offer them directly, white label solutions can provide an alternative route to access — though these may come with additional operational complexity and cost. Working with an advisor who actively monitors both direct and white label opportunities is essential to navigating the landscape and taking advantage of them when they arise.

The minimum investment threshold can be significant. Some Section 351 Exchange opportunities carry minimum contribution requirements that may limit accessibility for smaller portfolios.

Investors are subject to the risks of the newly created ETF. An investor will become a shareholder in the new ETF, and that means your money is tied to how the underlying investments perform. If those investments lose value, yours can too. Like any investment, the share price can go up and down with market conditions. If the ETF holds a narrow range of assets (rather than a broad mix), that concentration can amplify the swings. And while ETFs can generally be bought and sold on an exchange, there may be times when market conditions make that harder or more costly than expected.

The deferred gain does not disappear. Tax deferral is not tax elimination. When ETF shares are eventually sold, the deferred gain will be recognized. For investors planning to hold the ETF for the rest of their lives, the gain may be eliminated at death through a step-up in basis — but this outcome depends on future tax law and individual circumstances.

Structuring errors carry real consequences. Failure to meet the diversification test or errors in the structuring or documentation of the transaction can result in full taxable recognition of gains, significant penalties, and unexpected tax liabilities. The transaction requires specialized professional guidance familiar with both Section 351 requirements and ETF structures.

How Mason Approaches the Section 351 Exchange

Mason works closely with corporate executives who hold concentrated equity positions to evaluate whether a Section 351 Exchange is appropriate given their financial situation, tax profile, and long-term goals.

Our approach begins not with the transaction itself but with the broader planning context. How does this position fit within the executive’s retirement income plan? What is the after-tax outcome across different holding periods and market scenarios? How does the Section 351 Exchange compare to the other five strategies available for managing a concentrated position?

When a Section 351 Exchange is the right fit, we assist with identifying available opportunities, evaluating the diversification test for the specific basket of securities involved, and coordinating with the client’s tax and legal advisors to ensure proper structuring and documentation.

The result is a diversified ETF position that can serve as the foundation for a broadly diversified portfolio aligned with the client’s intermediate and long-term investment objectives.

Frequently Asked Questions About the Section 351 Exchange

What is a Section 351 Exchange?

A Section 351 Exchange is a transaction in which an investor contributes a basket of stocks, ETFs, or treasury bills into a newly created diversified ETF in exchange for shares of that ETF. Under Section 351 of the Internal Revenue Code, this exchange can qualify for tax-deferred treatment, meaning the investor does not recognize capital gains at the time of the contribution. The tax basis in the new ETF carries over from the contributed securities, and the deferred gain is recognized when ETF shares are eventually sold.

How do I qualify for tax-deferred treatment in a Section 351 Exchange?

To qualify for tax-deferred treatment, the basket of securities contributed must pass a two-part diversification test. No single stock may exceed 25% of the total contribution, and the top five stocks may not collectively exceed 50% of the total contribution. When ETFs are included in the contribution, the test looks through to the underlying holdings of those ETFs. Proper structuring and documentation are essential, as errors can result in full taxable recognition of gains.

What is the difference between a Section 351 Exchange and an exchange fund?

A Section 351 Exchange is a one-time transaction in which an investor contributes a basket of securities into a new diversified ETF, receiving ETF shares with a carried-over tax basis and no restrictions on when they can be sold. An exchange fund pools stock from multiple investors into a diversified fund, requires a seven-year lock-up period to maintain tax deferral, and must hold at least 20% of its assets in illiquid qualified assets. The Section 351 Exchange offers significantly more flexibility and liquidity than an exchange fund.

Can I contribute an ETF like QQQ into a Section 351 Exchange?

Yes. ETF positions can be included in the contribution basket for a Section 351 Exchange. For purposes of the diversification test, the ETF is looked through to its underlying holdings rather than treated as a single position. This means that a large position in a broadly diversified ETF like QQQ may help the overall basket meet the diversification requirements, even when combined with a significant individual stock position.

What happens to my tax basis after a Section 351 Exchange?

Your tax basis in the new diversified ETF equals the tax basis of the securities you contributed. The deferred gain is preserved in the ETF shares and will be recognized when you eventually sell those shares. If you hold the ETF until death, your heirs may receive a step-up in basis that eliminates the deferred gain, though this outcome depends on future tax law and individual circumstances.

Is the Section 351 Exchange always available?

No. Section 351 Exchanges are tied to specific ETF launches and are not continuously available. Opportunities arise periodically, and minimum contribution requirements may apply. Working with an advisor who actively monitors these opportunities is important for investors who want to take advantage of them when they arise.

If you are holding a concentrated position and are not sure where to start, the right first move is a conversation.

Click here to schedule a consultation with a Mason advisor >>

________________

Eric Rife, CFP®, CPWA®, is a Financial Planner at Mason Investment Advisory Services specializing in concentrated equity positions and executive compensation planning.

Thomas Pudner, CPA, CFA, CFP®, MST, is Co-Chief Investment Officer and Co-Director of Research at Mason Investment Advisory Services, where he has led investment research and portfolio strategy for 20 years.

This communication is for informational purposes and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Opinions and forward-looking statements expressed are subject to change without notice. Services are offered through Mason Investment Advisory Services, Inc. (“Mason”) an independent investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about Mason, including our investment strategies, fees, and objectives, is included in the Form ADV Part 2, which is available upon request. This is not an offer or solicitation for investment advisory services.

Investing involves risk, including possible loss of principal. Asset allocation and diversification may not protect against market risk, loss of principal or volatility of returns. There is no guarantee that any investment strategy discussed herein will work under all market conditions.

Section 351 exchanges into exchange-traded funds involve significant tax and investment risks that could result in substantial adverse consequences. Tax Risks: Failure to meet the strict diversification tests will trigger full taxable recognition of gains. Failure for a contributing portfolio to meet the 25/50 test will result in the exchange not qualify for tax-deferred treatment. This means the investor will be subject to immediate capital gains taxes on the appreciated assets being transferred. State tax laws may not conform to federal treatment, creating additional tax obligations. Investment Risks: An investor will become a shareholder in the ETF with exposure to underlying portfolio risks, market volatility affecting ETF share value, concentration risk if the ETF has limited diversification, and liquidity risk despite the ETF’s traded status if market conditions deteriorate. The transaction’s complexity requires specialized professional guidance familiar with both Section 351 requirements and ETF structures, as errors in structuring or documentation can result in complete disqualification of intended tax benefits, significant penalties, and substantial unexpected tax liabilities. No guarantee exists that intended tax treatment will be achieved, and changing tax laws or ETF regulations may adversely affect future benefits. This disclosure does not constitute legal or tax advice – consult qualified tax and legal professionals before proceeding.

Exchange funds require a minimum holding of up to seven years, during which an investment will be illiquid and an investor may not be able to withdraw funds. While an exchange fund is designed to provide diversification benefits, there is no guarantee that diversification will be achieved.