By Derek Lesnak, CFA®, CAIA®, Associate Investment Consultant and Senior Investment Analyst of Research, Mason Investment Advisory Services

The financial landscape has undergone a dramatic transformation since the Global Financial Crisis. According to Financial Times reporting, non-bank financial institutions now control over half of global financial assets for the first time since the pandemic, having grown at more than double the rate of traditional banks. This shift raises important questions about systemic risk, particularly as banks have become deeply intertwined with the shadow banking sector through various financing mechanisms. While private credit itself may not be large enough to trigger a systemic crisis independently, its growing interconnectedness with traditional banks creates channels through which shocks could be transmitted and amplified throughout the financial system.

The Rise of Shadow Banking: A Structural Shift in the Financial System

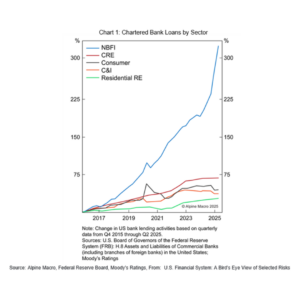

The financial system has been quietly reorganizing itself. Non-bank financial institutions, including insurance companies, private credit providers, money market funds, hedge funds, and securitization vehicles, have experienced explosive growth. Their asset base has expanded at a rapid pace compared to commercial real estate, traditional banking, business lending, and residential real estate.

This is not simply a story of growth in isolation. The post-crisis regulatory framework, designed to make banks safer through higher capital requirements and tighter risk controls, has inadvertently created powerful incentives for financial activity to migrate beyond the regulatory perimeter. Banks, constrained by these rules, have found creative ways to participate in riskier lending by financing the shadow banking entities that operate with fewer restrictions.

The International Monetary Fund and Federal Reserve have both flagged these developments as sources of hidden risk in fixed income markets. The IMF emphasizes that the ground is shifting beneath the financial system, creating new vulnerabilities that bear watching. While post-crisis reforms successfully forced banks to hold more capital and reduce direct risk-taking, banks have responded by increasing their lending to shadow banking entities, particularly private credit funds.

Why This Matters: The Interconnectedness Problem

The central concern is not necessarily that private credit is inherently dangerous. It is that lending has migrated from highly regulated banks to less regulated entities while maintaining deep financial linkages between the two sectors. While private credit and non-bank financial institutions may lack the standalone scale to generate systemic risk, their growing interconnectedness positions them as a potential transmission channel, capable of amplifying and propagating shocks that originate elsewhere in the financial system.

How Banks and Private Credit Funds Are Connected

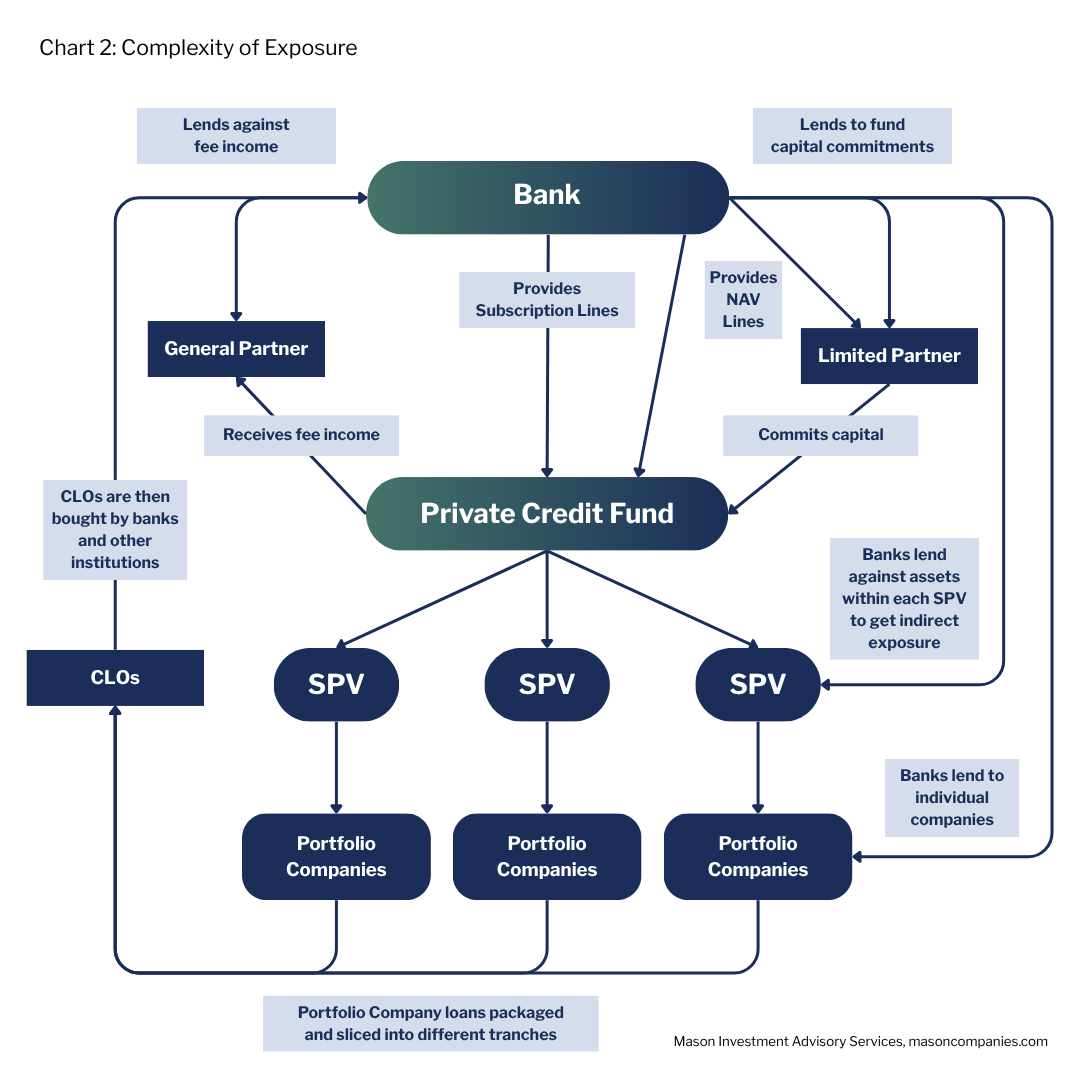

Understanding systemic risk requires mapping the specific channels through which banks and non-bank financial institutions have become entangled. These connections are both extensive and complex.

The Numbers Tell the Story

According to the Federal Reserve, bank lending to non-bank financial institutions has reached $1.2 trillion, with approximately $300 billion directed specifically to private credit. This lending has been the fastest-growing segment of bank loan portfolios since 2015, now accounting for over 10% of total US bank loans, triple the level from a decade ago according to Moody’s analysis.

History teaches us that liquidity crises can compound rapidly, exceeding even worst-case scenarios embedded in risk models.

The Complexity of Bank Exposure to Private Credit

The conventional wisdom holds that private credit failures may not trigger systemic shocks because this lending occurs outside the traditional banking system. Moody’s estimates direct private credit exposure at around $300 billion, or 1.5% of total bank assets. However, this figure likely understates true exposure because the relationship between banks and private credit is far more intricate than direct lending alone suggests.

Banks have effectively hitched their wagons to private credit through multiple mechanisms, allowing them to participate in the industry while ostensibly keeping their balance sheets clean and compliant with post-crisis regulations. They provide the leverage and liquidity that greases the wheels of the trillion-dollar private credit machine.

Investor Financing

Banks lend at multiple levels of the private credit structure. They provide loans to Limited Partners who need to fund their capital commitments to private credit funds. They lend to General Partners against future fee income they earn from the capital that Limited Partners have committed to their funds. Most significantly, they lend to the funds themselves through subscription lines.

Subscription Lines: The IRR Enhancement Tool

Subscription lines represent a particularly interesting dynamic. Private credit funds, measured by internal rate of return, will borrow from banks to make investments before calling capital from their investors. This timing arbitrage may enhance IRR calculations because returns are measured from when investor cash is deployed, not when the fund acquired the asset. A shorter measured hold period generates a higher IRR even though the fund owned the asset longer.

After deploying subscription line borrowings into loans to portfolio companies, private credit funds often return to banks seeking additional financing, using the very loans they just made as collateral. This creates a chain of leverage built upon leverage.

Bank Leverage Through Special Purpose Vehicles

Banks typically structure their funding of private credit lending to Special Purpose Vehicles. These SPVs give banks indirect exposure to the ultimate borrowers of private credit funds while providing a legal structure that facilitates ring fencing, the separation of specific asset pools as distinct collateral packages.

The private credit fund owns the equity in these SPVs, but the SPVs operate as separate legal entities. A single fund may establish multiple SPVs when receiving leverage from different banks. While these loans typically feature over-collateralization as a protective measure, rapid deterioration in loan performance could still generate losses for banks even on over-collateralized positions.

Repo Financing: Hidden in Plain Sight

Repo financing adds another layer of opacity to bank exposure. A private credit fund’s SPV can sell a portfolio of loans to a bank with an agreement to repurchase them later at a predetermined price. These transactions obscure the true scale of bank involvement in private credit because they operate in the shadows of public disclosure.

The repo market traditionally serves to meet short-term funding needs for financial institutions. Tying repos to illiquid private credit debt creates potential systemic risk, particularly if funding markets freeze during periods of stress.

NAV Loans: What They Are and Why They Matter

Net Asset Value loans represent perhaps the most concerning form of interconnection. These loans, backed by the overall value of a fund, provide liquidity to investors seeking early exits or funds looking to invest more. They effectively layer leverage upon leverage, borrowing against a portfolio that was itself funded substantially through borrowing.

One key risk: the assets inside these funds, such as private loans and direct lending deals, do not trade on a public exchange the way stocks or bonds do. That means there is no real-time market price to point to. Instead, valuations are based on estimates and models, which introduces a degree of subjectivity. This becomes especially important in NAV lending, where the loan is secured by the fund’s reported net asset value. If that NAV turns out to be overstated, the collateral backing the loan may not be worth as much as it appears on paper.

Direct Lending to Portfolio Companies

Banks also maintain the option to lend directly to the underlying portfolio companies held by private credit funds, creating yet another connection point.

Collateralized Loan Obligations (CLOs)

Private credit funds pool their loans and sell them through CLOs to institutional investors including insurance companies, pension funds, hedge funds, and banks. The circularity is notable: many of these investors are simultaneously investing directly in private credit funds themselves.

Risk Transfer Mechanisms

Banks have recently begun using significant risk transfers to shift exposure off their balance sheets. These transactions involve repackaging loans and purchasing default protection on the riskiest tranches from investors who receive quarterly fees in exchange for bearing default risk.

While traditionally used for conventional corporate and mortgage debt, banks have begun extending these structures to private credit exposures. Critics worry this merely shuffles risk around the financial system rather than genuinely reducing it.

Assessing the Current Health of Private Credit Markets

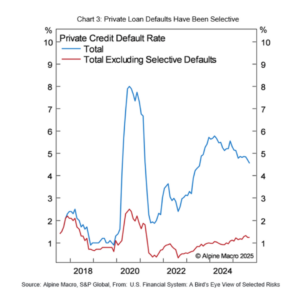

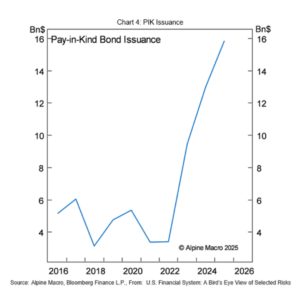

Current default rates in private credit stand around 4.5%, higher than the late 2010s but declining. Most defaults are selective defaults: situations where companies exchange existing debt for restructured debt or make equity payments in kind. Typically, this involves interest payment deferrals or maturity extensions that provide insufficient compensation to creditors. PIK issuance has taken off since 2022.

Selective defaults, while less severe than traditional defaults, reduce ultimate recovery rates when hard defaults eventually occur. Traditional default rates remain low at 1% but have been trending upward.

Recent high-profile failures have attracted attention from Wall Street leadership. The collapses of fraudulent companies like Tricolor and First Brands Group prompted JPMorgan CEO Jamie Dimon to refer to them as “cockroaches,” suggesting that visible problems indicate hidden ones. Concerns center on the fact that much CLO collateral remains unrated, raising questions about whether due diligence has taken a backseat to deal execution. The financial crisis taught us what happens when collateralized products are structured hastily with limited diligence.

The CLO market has expanded rapidly, fueled by both private credit and private equity transactions, with some structures reaching 10 times leverage according to Financial Times reporting. While most CLO metrics currently appear stable, downgrades have accelerated over recent quarters, albeit from very low baseline levels.

Early Cracks in 2026

There have been small cracks forming in the private credit ecosystem to start 2026, according to our recent analysis. Four of the five largest private credit funds available to everyday investors came under serious strain as too many investors tried to pull their money out at once. The most dramatic example came on February 18, 2026, when Blue Owl Capital froze redemptions and sold roughly $600 million in loans, about a third of its portfolio, at a small discount. Morningstar described the move as an effective wind-down of the fund.

Several other funds have begun limiting how much investors can withdraw, capping redemptions at just 5 to 7% of fund assets per quarter. In practice, investors are only receiving about half of what they have asked to take out. BlackRock and Cliffwater, for example, received withdrawal requests totaling 9.3% and 14% of their funds, respectively, far more than they could honor in full.

Does Private Credit Pose Systemic Risk? What the Data Says

The bankruptcies of First Brands Group and Tricolor appear to be isolated events at present, but they illustrate how private credit deals can unwind badly. The transactions private credit funds pursue may be too risky for banks to execute directly under current regulations, yet private credit may not pose as much systemic risk as feared because these funds employ less leverage than banks in many cases. Additionally, traditional private credit funds benefit from long lock-up periods and limited withdrawal activity, which may substantially reduces run risk.

According to IMF analysis, a worst-case scenario involving an unexpected economic shock would result in approximately 15% of US banks facing liquidity stress. This suggests meaningful but manageable vulnerability under severe conditions.

What This Means for Institutional Investors

The risks building within the shadow banking system warrant close monitoring but have not yet reached crisis proportions. The private credit market remains too small to independently trigger systemic failure, but its dense interconnections with traditional banks create transmission channels through which shocks could propagate and amplify.

The financial system has become more complex and opaque as activity has migrated beyond the regulatory perimeter. While this evolution has brought benefits including greater lending capacity and risk distribution, it has also created new vulnerabilities that policymakers and market participants must understand and manage.

For foundations, endowments, and institutional portfolios being actively pitched private credit as an alternative allocation, the key questions to bring to your investment committee include these: How exposed is the portfolio to the interconnections described above? Are valuations being stress-tested against conditions beyond normal market cycles? And how does liquidity within private credit positions align with the institution’s actual spending and redemption needs?

Mason’s investment research team continues to monitor developments in private credit markets and their implications for institutional and private client portfolios.

Frequently Asked Questions About Private Credit Risk

What is private credit and how does it work?

Private credit refers to loans made by non-bank lenders, including private credit funds, insurance companies, and institutional vehicles, directly to companies outside the public debt markets. Borrowers typically access private credit when they need speed, flexibility, or capital that traditional banks cannot efficiently provide under post-crisis regulatory frameworks. Private credit funds pool capital from institutional and increasingly retail investors and deploy it as loans, earning interest income that is passed through to investors.

Is private credit a systemic risk to the banking system?

Private credit may be unlikely to trigger a systemic crisis independently, given its size relative to the broader financial system. However, its dense interconnections with traditional banks, through subscription lines, special purpose vehicles, repo financing, NAV loans, and CLOs, create channels through which shocks could be transmitted and amplified. The IMF estimates that a severe economic shock could put approximately 15% of US banks under liquidity stress, in part due to these interconnections.

What happened with Blue Owl Capital in February 2026?

On February 18, 2026, Blue Owl Capital reportedly froze redemptions on its retail-accessible private credit fund and sold approximately $600 million in loans, roughly one third of its portfolio, at a discount to meet investor withdrawal requests. Morningstar described the event as an effective wind-down of the fund. Several other large private credit funds including those managed by BlackRock and Cliffwater subsequently capped redemptions at 5 to 7% of fund assets per quarter, leaving investors receiving approximately half of what they requested.

What is a NAV loan in private credit?

A Net Asset Value loan is a loan secured by the overall value of a private credit fund rather than by specific underlying assets. NAV loans provide liquidity to investors seeking early exits or to funds seeking to deploy additional capital. They are considered among the more complex forms of bank-private credit interconnection because they layer leverage upon leverage, borrowing against a portfolio that was itself substantially funded through borrowing. Because private credit assets are valued through models rather than real-time market prices, the collateral backing a NAV loan may be worth less than it appears if fund valuations are overstated.

What is the current private credit default rate?

As of the most recent available data, total default rates in private credit stand at approximately 4.5%, with hard defaults at approximately 1% and the balance representing selective defaults including restructurings, debt exchanges, and payment-in-kind arrangements. Traditional default rates have been trending upward from historically low levels, while selective defaults have increased substantially since 2022.

______________

Derek Lesnak, CFA®, CAIA®, is an Associate Investment Consultant and Senior Investment Analyst of Research at Mason Investment Advisory Services, where he contributes to the firm’s investment research and portfolio strategy functions.

The information provided in this article is for educational purposes only and does not constitute investment advice or a recommendation of any particular security, strategy, or investment product. Opinions expressed reflect the current views of the author as of the date of publication and are subject to change without notice. The charts and/or graphs contained herein are for educational purposes only and should not be used to predict security prices or market levels. Information is based on data gathered from what we believe are reliable sources. It is not guaranteed as to accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor. Past performance is not indicative of future results. Please consult a qualified financial advisor regarding your specific situation.