By Margo Steinlage, Co-Owner, President and Independent Broker, Steinlage Insurance Agency, and Blaine Homan, CFP®, Mason Investment Advisory Services

Most people approaching retirement assume Medicare Part B costs roughly $200 a month. For many Americans, that is accurate. For high earners, it is not even close.

If your income exceeds certain thresholds, Medicare adds a surcharge to your Part B and Part D premiums called IRMAA — the Income-Related Monthly Adjustment Amount. Depending on your income, IRMAA can push your Part B premium from $202.90 per month to as high as $689.90 per month. Per person. That is before any Part D surcharge is layered on top (additional $91/month/person).

What makes IRMAA particularly disruptive is when people find out about it. Not before retirement, when there is still time to plan. Not even at enrollment. Most people discover IRMAA when the bill arrives and it is higher than they expected.

This guide explains exactly how IRMAA works, what income triggers it, how the appeal process works, and how the financial planning decisions you are making right now may be setting your Medicare premiums two years from today.

What Is IRMAA? A Plain-Language Explanation

IRMAA stands for Income-Related Monthly Adjustment Amount. It is a premium surcharge added to Medicare Part B (medical coverage) and Medicare Part D (prescription drug coverage) for beneficiaries whose income exceeds a set threshold.

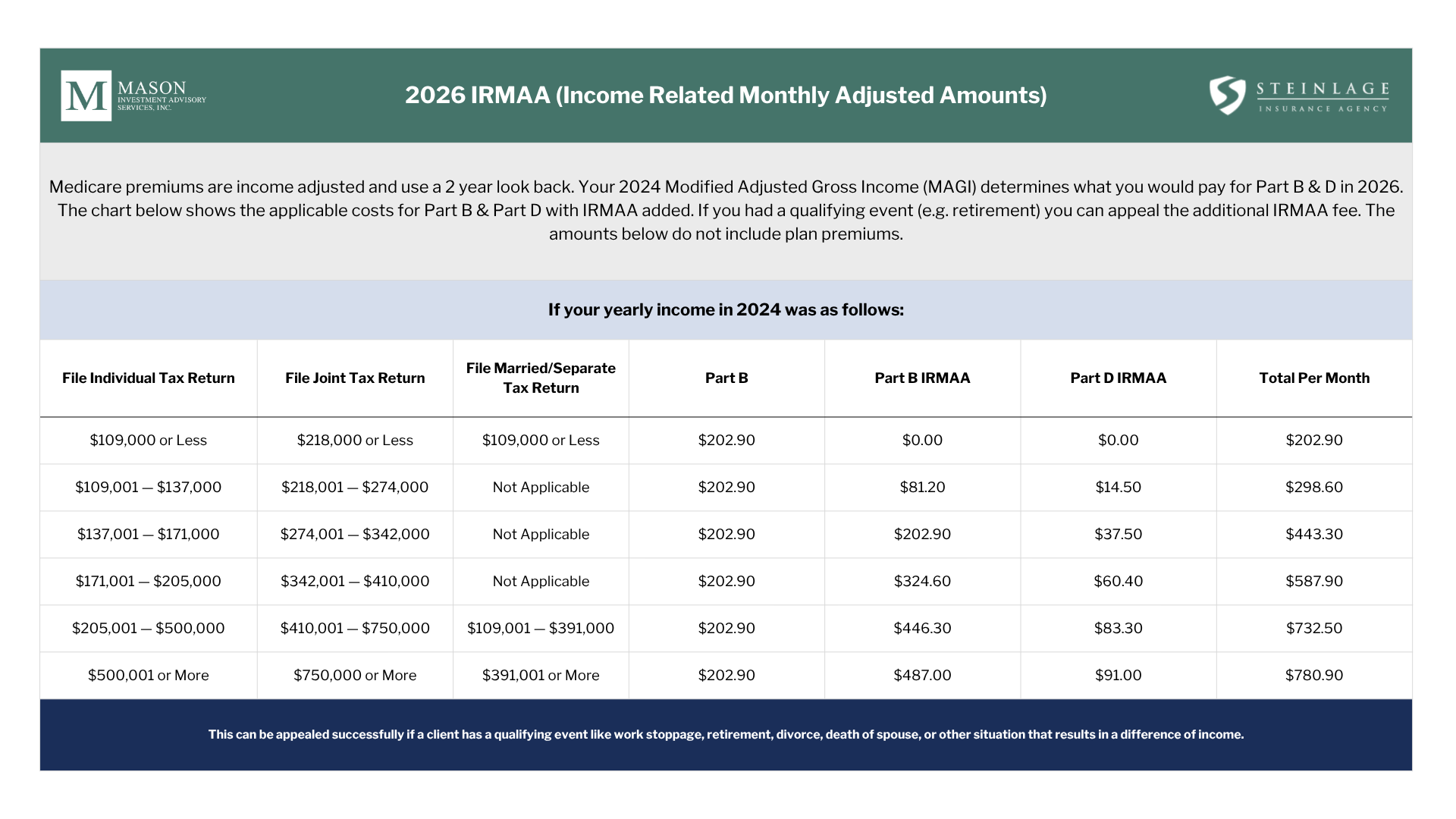

Medicare uses a two-year lookback to calculate your IRMAA. That means your 2026 Medicare premiums are based on your 2024 Modified Adjusted Gross Income (MAGI) as reported on your 2024 federal tax return. If you retired in 2025 and your income dropped significantly, Medicare does not automatically know that. It is still looking at 2024.

This two-year lag is the source of most IRMAA surprises. A high-earning executive retires. Income drops. But for the first year or two on Medicare, premiums reflect the income from their final working years. Without a proactive appeal, they pay the higher rate.

What Is the Income Limit for IRMAA?

For 2026, see the chart below for the IRMAA income limits.

Note: Part D carries a separate IRMAA surcharge ranging from approximately $14 to $91 per month depending on income tier. IRMAA brackets are updated annually. Confirm current-year figures at ssa.gov.

One detail worth emphasizing: IRMAA brackets are not progressive in the way income tax brackets are. If your income lands one dollar over the threshold into the next bracket, your entire premium adjusts to that bracket’s rate — not just the income above the line. Being close to a bracket ceiling is not a small thing. A modest income difference can mean hundreds of dollars more per year.

Does Social Security Count as Income for IRMAA?

This question comes up often, and the answer matters for retirement income planning.

IRMAA is calculated on Modified Adjusted Gross Income, which includes:

- Wages and self-employment income

- Capital gains (short-term and long-term)

- Dividends and interest

- Rental income

- Required Minimum Distributions (RMDs)

- Up to 85% of Social Security benefits, if your total income exceeds certain thresholds

- Roth conversion income

- Business income

Social Security itself is not always fully counted — the amount included in your MAGI depends on your overall income level — but for most high earners in retirement, a portion of Social Security benefits will factor into the IRMAA calculation. Assuming Social Security is irrelevant to IRMAA is one of the planning errors we see most often.

What Most People Get Wrong About IRMAA

The most common IRMAA mistake is not a math error. It is an information gap. People simply do not know it exists until it shows up on a premium notice.

The second most common mistake is a planning blind spot: income decisions made before retirement that create IRMAA exposure after it. A Roth conversion executed in December. A home sale that generates a large capital gain. An equity event — stock options, restricted stock units, a buyout — that produces a one-time income spike. These transactions can push MAGI above an IRMAA threshold in the lookback year, and the premium consequence follows the retiree into Medicare regardless of what their ongoing income looks like.

A third mistake: assuming IRMAA is fixed. It is not. It can be appealed, reduced, or removed entirely — but only if you know the rules and act on them.

What Financial Decisions Trigger Higher IRMAA?

For high earners and retirees with complex financial pictures, several common planning moves can increase MAGI and push premiums into a higher IRMAA tier:

- Roth Conversions Converting a traditional IRA or 401(k) to a Roth account is a powerful long-term tax strategy. But conversion income counts as MAGI in the year it is executed, which can trigger or worsen IRMAA two years later. The timing of conversions relative to Medicare enrollment requires careful modeling — particularly in the years immediately before and after retirement.

- Home Sales A capital gain from a home sale, net of the $250,000/$500,000 exclusion, is included in MAGI. For clients with high-value real estate in appreciated markets, the gain above the exclusion can be substantial enough to push MAGI into a higher IRMAA bracket.

- Required Minimum Distributions RMDs begin at age 73 under current law and are treated as ordinary income. For clients with large pre-tax retirement accounts, RMDs can keep MAGI elevated well into retirement even after wages stop entirely. This is one reason Roth conversion strategy in the years before RMDs begin deserves serious attention — though the IRMAA timing implications must be part of that analysis.

- Equity Compensation Events Executive compensation — stock options, RSUs, deferred compensation payouts, or business buyouts — can produce significant one-time income. If that event falls in a lookback year, the IRMAA impact arrives at enrollment and can persist for years.

Note: A lump-sum buyout can sometimes work in the opposite direction. In certain situations, accepting an upfront payment triggers IRMAA for one or two years rather than the sustained IRMAA exposure that results from a multi-year payout structure. This is a situation where running the numbers with your financial advisor before accepting the offer structure is worthwhile.

How to Avoid IRMAA (or Minimize It)

Avoiding IRMAA entirely is not always realistic, particularly for clients with significant pre-tax accounts and ongoing investment income. But reducing it — or eliminating it in years where income drops — is often achievable with the right planning.

- Plan MAGI-impacting decisions with IRMAA brackets in mind. If a Roth conversion or asset sale is going to push income over a threshold, the question is whether the long-term benefit justifies the near-term Medicare premium cost. Sometimes it clearly does. Sometimes the math looks different than expected.

- Use current-year IRMAA brackets when projecting, but do not obsess over precision. The brackets adjust annually, and projecting two years out involves estimates. Margo’s approach: use a conservative income assumption when you are near a bracket threshold. If you underestimate and owe more, Medicare and Social Security will true up the difference. If you overestimate and pay more than you owed, Medicare will not refund the overpayment.

- Appeal when income drops. The most actionable form of IRMAA management for most retirees is a timely appeal when a qualifying life event causes income to fall. That process is covered in detail below.

How to Appeal IRMAA: The SSA-44 Form and Qualifying Life Events

If your income has dropped since the lookback year due to retirement, death of a spouse, divorce, or another qualifying event, you can request that Medicare use your current or anticipated income instead of the two-year lookback figure. This is done by filing Form SSA-44.

The Three Most Common Qualifying Life Events for an IRMAA Appeal

- Retirement or reduction in work. If you stopped working or significantly reduced your hours, you can request that Medicare project your current income instead of using your final working years’ tax return.

- Death of a spouse. If your spouse was the higher earner and they have passed, your MAGI from the joint return no longer reflects your current financial situation. An appeal using current anticipated income is appropriate.

- Divorce from a high-earning spouse. If divorce has materially changed your income picture, that qualifies as a life event that supports an IRMAA appeal.

Other qualifying events include loss of income-producing property that was not at your direction , loss of pension income, and employer settlement payments. If there is any question about whether your situation qualifies, it is worth filing. There is no penalty for appealing IRMAA.

How the SSA-44 Process Works

To appeal, you complete Form SSA-44 (available at ssa.gov) and submit documentation supporting the qualifying life event and your anticipated income for the current year if you can produce income documentation. Most clients will only have proof of the qualifying life event (divorce decree, retirement letter) and proof of the life event will suffice. Other documents used to prove the life event (most important) and if available income based on the life event includes:

- For retirement: a letter from your employer confirming your last day of employment, or a self-employed statement on letterhead describing the work reduction

- For death of a spouse: a death certificate

- For divorce: a divorce decree

- For income projections: supporting documentation showing anticipated MAGI for the year in question

If documentation is unavailable, filing the SSA-44 alone is generally better than not filing. The Social Security Administration may still consider the request.

One detail that surprises many couples: if both spouses are on Medicare, each must file a separate SSA-44. There is no joint appeal. Even if your income is reported on a single joint tax return, the Social Security Administration processes each beneficiary individually. Both forms need to be filed.

What Happens After You File

Once filed, the SSA will review your request and notify you of the determination. If your appeal is approved, your premium will be adjusted going forward. If your actual income for the projected year ends up higher than what you anticipated, Medicare and Social Security will communicate and adjust the difference — you will owe the additional amount. There is no penalty for estimating conservatively and coming in above it.

The one asymmetry worth understanding: Medicare does not issue refunds if you paid more IRMAA than you ultimately owed. If you overpaid because your income came in lower than projected, that excess does not come back. This is another reason Margo recommends filing aggressively when circumstances support it. There is no downside to requesting relief. The worst outcome is that the appeal is denied and you continue paying the assessed rate.

At Mason, Blaine and the advisory team have worked alongside clients to prepare and file the SSA-44. Navigating the Social Security Administration is easier when someone who knows the process is sitting across the table from you.

IRMAA and Tax Planning: Questions High Earners Ask

Can I Deduct My Medicare Part B Premiums on My Taxes?

Yes, in certain circumstances. Medicare Part B and Part D premiums are treated as medical expenses for federal income tax purposes. If you itemize deductions and your total unreimbursed medical expenses exceed 7.5% of your adjusted gross income, the amount above that threshold is deductible.

In practice, however, high earners are often the least likely to benefit from this deduction. The 7.5% hurdle scales with income — a retiree with $1 million in AGI would need more than $75,000 in unreimbursed medical expenses before a single dollar becomes deductible. The deduction tends to be most meaningful for lower-income retirees who incur significant medical costs, or for clients who make a large buy-in payment to a continuing care retirement community (CCRC), a portion of which is typically designated as a qualified medical expense. For high-IRMAA payers, the medical expense deduction is unlikely to provide meaningful relief, but it is worth reviewing annually with your tax advisor — particularly in years with extraordinary health-related costs.

Self-employed individuals may have an additional pathway: the self-employed health insurance deduction allows Medicare premiums to be deducted directly from gross income, above the line, without needing to itemize or meet the 7.5% threshold.

What Is the $6,000 Tax Deduction for Seniors?

The $6,000 figure refers to a new, temporary enhanced deduction for seniors created under the One Big Beautiful Bill Act, signed into law on July 4, 2025. It is a separate deduction — in addition to the existing age-based additional standard deduction — and is available to taxpayers age 65 or older for tax years 2025 through 2028.

The deduction is $6,000 per qualifying individual, or $12,000 for a married couple filing jointly where both spouses are 65 or older. It is available to both those who itemize and those who take the standard deduction, which makes it broader in application than many deductions.

The critical caveat for Mason’s clients: the deduction phases out for taxpayers with MAGI above $75,000 for single filers and $150,000 for joint filers. For high earners — particularly those in IRMAA territory — this deduction is largely or entirely phased out. It is worth confirming the math with your advisor, but most clients managing IRMAA exposure may not see meaningful benefit from this provision.

The standard age-based additional deduction also continues in parallel. For 2026, that additional deduction is $2,050 for single filers and $1,650 per qualifying spouse for joint filers. Unlike the $6,000 enhanced deduction, there is no income phase-out on the age-based additional deduction.

Neither deduction directly reduces IRMAA, which is calculated on MAGI before deductions are applied. But both reduce taxable income, which has downstream planning implications worth reviewing annually.

Note: Tax figures change annually. Confirm current-year amounts with your advisor or at irs.gov.

What Is the Most Overlooked Tax Deduction in Retirement?

In the context of Medicare planning, the most consistently overlooked deduction is the Medicare premium deduction itself — particularly for retirees who are paying elevated IRMAA surcharges and may be accumulating meaningful medical expenses.

The broader tax planning mistake in retirement is not a single overlooked deduction. It is the failure to model the relationship between income management and Medicare costs. Every dollar of income in the lookback year has a Medicare premium consequence two years later. Many retirees manage their income for tax purposes without ever running that calculation. Coordinating with a financial advisor who considers both dimensions simultaneously can produce a meaningfully different outcome.

What Are the Biggest Medicare Mistakes High Earners Make?

Based on what we see in practice — and the questions that came up during our live webinar — here are the most common and costly Medicare mistakes:

- Not knowing IRMAA exists. IRMAA is not prominently communicated at enrollment. Most people encounter it for the first time when they receive their premium notice. By then, the income that triggered it is already two years in the past.

- Ignoring the two-year lookback when making financial decisions. Roth conversions, home sales, business transactions, and equity events in the two years before Medicare enrollment can produce IRMAA exposure that persists for years. These decisions should be modeled with Medicare costs in mind, not in isolation.

- Assuming IRMAA is permanent. It is not. For retirees whose income drops after they leave the workforce, an appeal using the SSA-44 form can reduce or eliminate the surcharge. Many people pay elevated premiums for years without knowing the appeal option exists.

- Not filing a separate SSA-44 for each spouse. Couples sometimes assume one appeal covers both. It does not. Each beneficiary must file individually.

- Overestimating income in the appeal and losing the overpayment. If you file an SSA-44 with a projected income figure that turns out to be too low, Social Security will true up the difference. If your actual income comes in lower than projected and you overpaid, Medicare will not refund the excess. The recommendation is to appeal with a conservative income projection when you are near a bracket threshold.

- Waiting too long to plan. IRMAA is not a retirement problem. It is a pre-retirement planning problem. The income decisions made in the two to three years before Medicare enrollment set the premium table. Starting the conversation with your advisor before those decisions are made is the most effective form of IRMAA management.

The Bottom Line on IRMAA

IRMAA is not a Medicare tax or penalty. It is a surcharge tied to income — one that can add thousands of dollars per year to Medicare costs for high earners, and one that is largely invisible until it arrives.

The good news is that it is plannable. With the right information, the right timing, and an advisor who treats Medicare costs as part of the overall retirement income plan, IRMAA can be anticipated, reduced, and in some circumstances appealed out entirely.

For most of the clients we work with, the interaction between retirement income planning and Medicare premium costs is not a footnote. It is a central variable in building a retirement that is financially sustainable and free of avoidable surprises.

Work With a Team That Sees the Whole Picture

Medicare planning and financial planning are not separate conversations. For high earners, the decisions your financial advisor makes — and the timing of those decisions — directly determine what you will pay for Medicare coverage.

At Mason, our advisors work alongside Medicare specialists like Margo Steinlage to help clients make decisions that account for the full picture: income, taxes, Medicare costs, and long-term financial goals. We have helped clients file SSA-44 appeals, model the IRMAA impact of Roth conversions, and structure retirement income to minimize unnecessary premium exposure.

For Medicare coverage questions and IRMAA guidance, contact Margo Steinlage at Steinlage Insurance Agency: margo@steinlageinsurance.com.

For questions about how IRMAA and Medicare costs fit into your retirement income strategy, click here to schedule a consultation with a Mason advisor >>

For a broader overview of Medicare enrollment decisions, read our companion post: Your Medicare Enrollment Questions Answered: What We Heard at Our Live Webinar.

The information in this article is for educational purposes only and does not constitute financial, legal, or tax advice. Medicare rules, premium amounts, and IRMAA brackets are subject to change annually. Please consult a qualified Medicare specialist and financial advisor regarding your specific situation.